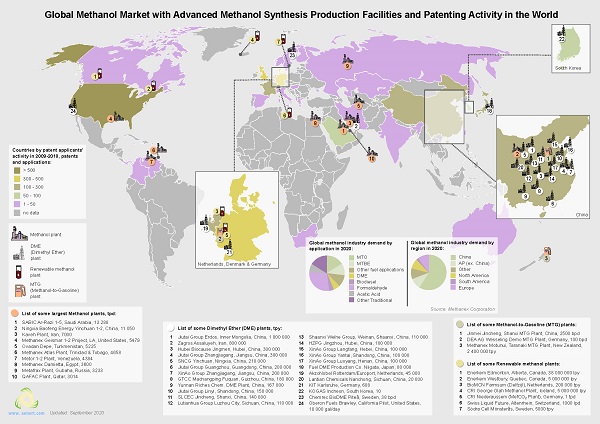

Methanex is the world’s largest producer and supplier of methanol to the major international markets in Asia Pacific, North America, Europe and South America. The total annual operating capacity, including Methanex’s interests in jointly owned plants, is 9.2 million tonnes in 2020 and is located in New Zealand, the United States, Trinidad, Chile, Egypt, and Canada.

In 2020, global methanol demand fell significantly in the first half due to impacts from the COVID-19 pandemic and lower oil price environment and totalled approximately 82 million tonnes in 2020, reflecting a 3% decrease compared to 2019.

Traditional chemical demand declined by approximately 5% year-over-year due to lower manufacturing activity as a result of impacts from the COVID-19 pandemic. Demand into energy-related applications was flat year-over-year.

There is growing interest in methanol as a marine fuel given its environmental benefits and cost competitiveness as well as a vehicle fuel due to its emissions benefits. Approximately 60% of Methanex´ long-term shipping fleet, or 19 vessels in total, will have the capability to run on methanol by 2023.

According to the company´s Annual Financial Report, Methanex reported a net loss attributable to Methanex shareholders of $157 million or $2.06 loss per common share at the end of 2020, compared with net income attributable to Methanex shareholders of $88 million or $1.01 income per common share in 2019 and $569 million or $6.92 income per common share in 2018.

In 2020, the company achieved adjusted EBITDA of $346 million and adjusted net loss of $123 million or $1.62 adjusted net loss per common share, compared with Adjusted EBITDA of $566 million and adjusted net income of $71 million or $0.93 adjusted net income per common share in 2019 and adjusted EBITDA of $1,071 million and adjusted net income of $556 million in 2018. In 2020 the adjusted EBITDA decreased by $220 million year-over-year. The key drivers of change in adjusted EBITDA are average realized price, sales volume and cash costs.

Revenue of the company had a decrease of 22% from $3.3 billion in 2019 to $2.5 billion in 2020, compared with $4.5 billion revenues achieved by Methanex in 2018.

There are many factors that impact global and regional revenue. Decreased demand for methanol is driven by a number of factors including industrial production levels, energy prices, pricing of end products, government regulations and policies. The lower revenue reflects a lower average realized price in 2020 compared to 2019.

The average non-discounted published reference price in 2020 was $297 per tonne compared with $353 per tonne in 2019 and the average realized price in 2020 was $247 per tonne compared to $295 per tonne for 2019, and this factor alone decreased adjusted EBITDA by $468 million.

In 2020, the methanol sales volume decreased by 0.4 million tonnes from 10.1 million tonnes in 2019 to 9.7 million tonnes in 2020, and this decreased adjusted EBITDA by $28 million. Including commission sales volume from the Atlas and Egypt facilities, total methanol sales volume of the Company was 10.7 million tonnes in 2020 compared with 11.1 million tonnes in 2019. The sales volume was lower for 2020 compared to 2019 primarily due to the impact of COVID-19 on methanol demand globally.

Methanex-produced methanol costs were lower by $225 million in 2020 compared with 2019, primarily due to the impact of lower realized methanol prices on natural gas costs.

Lower purchased methanol prices in 2020 decreased the cost of purchased methanol per tonne and this increased adjusted EBITDA by $136 million compared with 2019.

Cash flows from operating activities for the year ended December 31, 2020 were $461 million compared with $515 million in 2019 and with $980 million for the year 2018. The decrease of almost 11% in cash flows from operating activities is primarily due to lower earnings.

As of December 31, 2020, the company had a cash balance of $834 million compared to $417 million in 2019, including $77 million of cash related to Egypt entity and $8 million of cash related to its joint venture interests in ocean going vessels.

In April 2020, the company announced the deferral of approximately $500 million of the planned capital budget for the Geismar 3 project, a 1.8 million methanol plant, for up to 18 months.

The planned operational capital expenditures directed towards maintenance, turnarounds, and catalyst changes, including 63.1% share of Atlas and 50% of Egypt, are currently estimated to be approximately $110 million for 2021.

Growing interest in clean-burning fuels and regulatory changes are playing an increasing role in encouraging new applications for methanol as a fuel due to its lower emissions.

Energy News Monitoring

METHANEX CORPORATION 2020

Further decrease of revenue and income in 2020